Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Lately we have talked about life changes leading to real estate moves. Sometimes moves are brought on by joyful advancements in life and sometimes they are motivated by hardship. Then there are times when your actual house just doesn’t fit your life anymore and it is time for something different. Whatever might be calling someone to make a move, they also have to assess the affordability.

There are three aspects to affordability: price, interest rate, and income. Price and interest rate will determine your monthly payment, and your income will provide the means to maintain and build your investment. One way I have been able to help my clients strategize affordability with higher interest rates are some creative financing options.

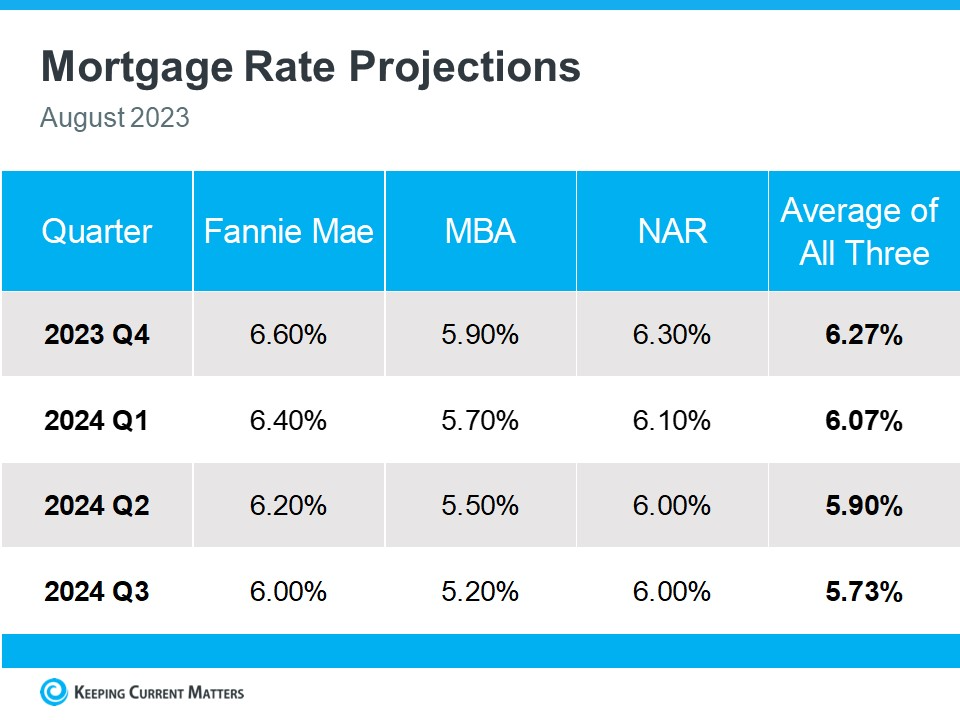

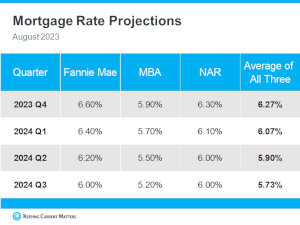

Most often a home buyer will procure a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens.

Most often a home buyer will procure a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens.

I have helped some of my clients overcome the higher interest rates and secure today’s prices by helping them arrange with their lender an interest rate buy-down. Sometimes we have even been able to get the seller to financially assist in paying for the buy-down. There are two types of buy-downs: a permanent buy-down and a temporary buy-down.

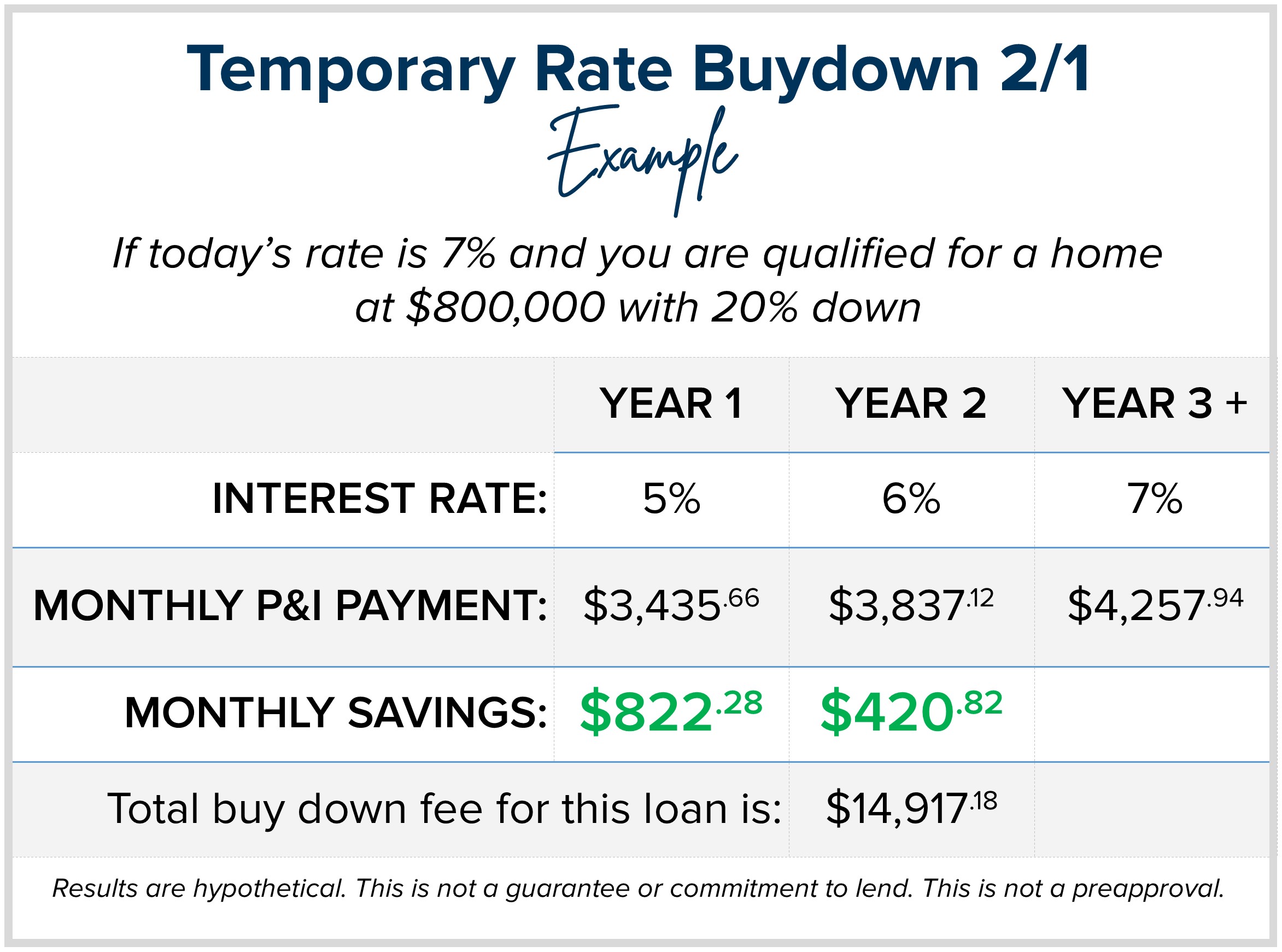

A permanent buy-down requires about 3% of the purchase price to buy the rate down by a point for the 30-year term of the loan. A good rule of thumb to remember is that every 1-point in rate equals 10% in buying power. For example, if the rate is 7% and you are qualified for a home at $800,000, if the rate went down by 1 point to 6% you could now afford $880,000 and have a very similar payment. Another way to look at this is simply the monthly payment itself. An $800,000 purchase with 20% down with a 6% interest rate would save a buyer $420.82 a month vs. the payment at 7%.

A permanent buy-down is a useful tool and so is a temporary buy-down. It is actually one of the most powerful tools in today’s market. It costs far less than a permanent buy-down and with rates predicted to decrease over the next 12-18 months as inflation settles, you could easily find yourself in a position to refinance.

Here is an example, let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

Here is an example, let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

The roughly $15,000 in monthly payment savings is paid upfront at closing and in some cases paid by the seller. The buyer still needs to qualify based on the 7% interest rate as the payments will convert to the payment based on the 7% in year three moving forward. The strategy here is to never have the payment increase to 7% amount because the buyer plans to refinance when rates come down and will permanently fix their rate below 7%. A bonus is that if the entire $15,000 credit has not been used yet, in some cases those funds can be applied towards the refinance.

This strategy has been effective in helping buyers secure a monthly payment that is more affordable so they can make a move now based on life’s needs and wants. It also helps them secure today’s prices. If we find a home that has had a little longer market time, a home seller is likely to assist with the $15,000 credit vs. reducing their price by 3% to accommodate a lower payment for 30 years. The temporary assistance in reducing the payment for 1 to 2 years is a viable tool for both the buyer and seller to create a win-win.

I felt it was important to bring these options to light and to encourage people to not just take today’s market at face value. Creativity, collaboration, and calm have led to some of the most rewarding sales this year for both buyers and sellers. When people logically work together to accomplish moves in an environment that seems difficult, they find success. Ultimately, I am here to help my clients match their real estate to their lives despite where the rates are today.

I love rolling up my sleeves and creating a plan to help my buyers and sellers accomplish their goals. It is my mission to help keep my clients informed and empower strong decisions. If you or someone you know are curious about how today’s market matches your needs, please reach out.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

Thank you!

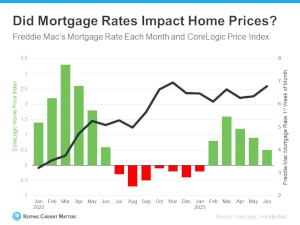

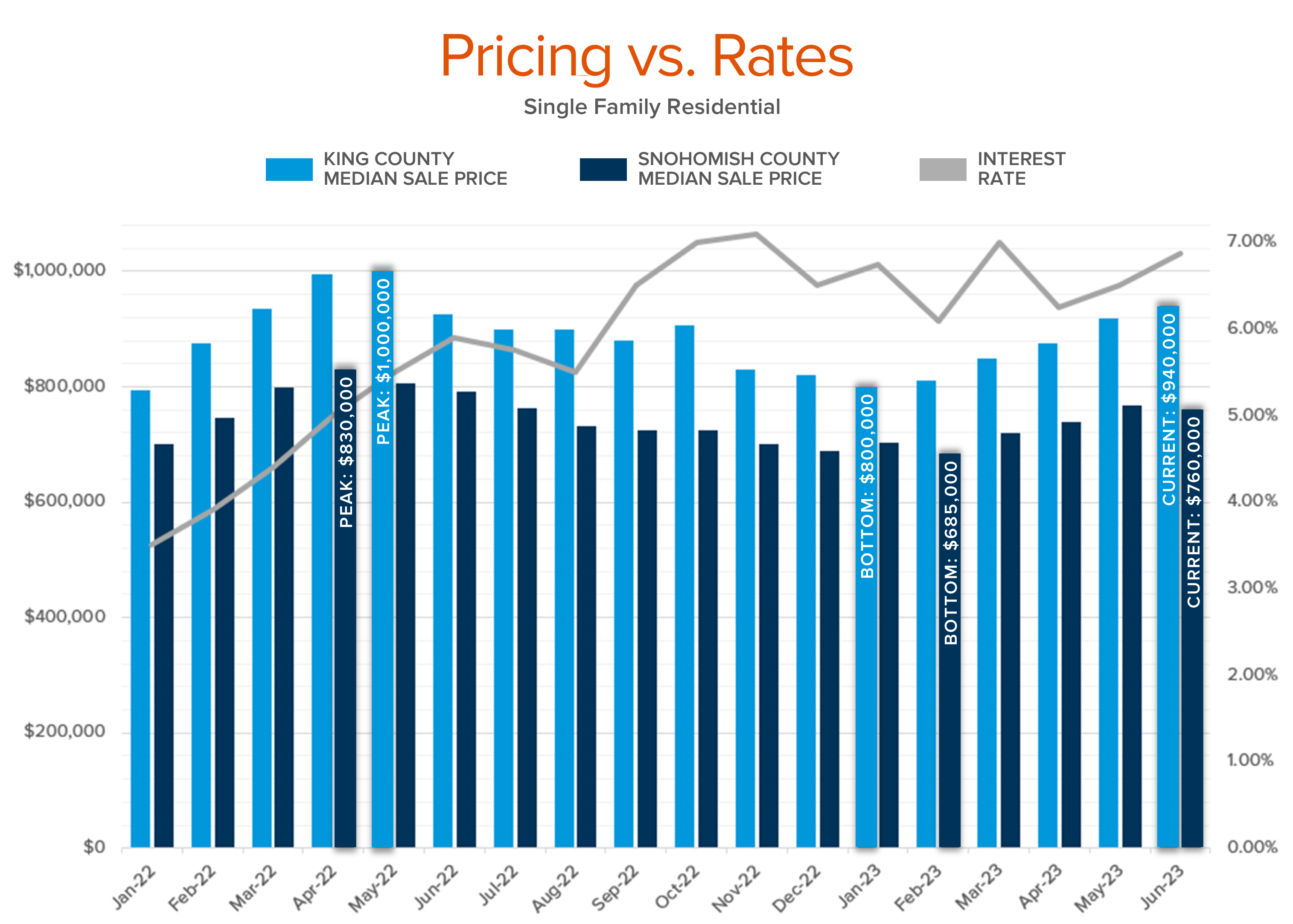

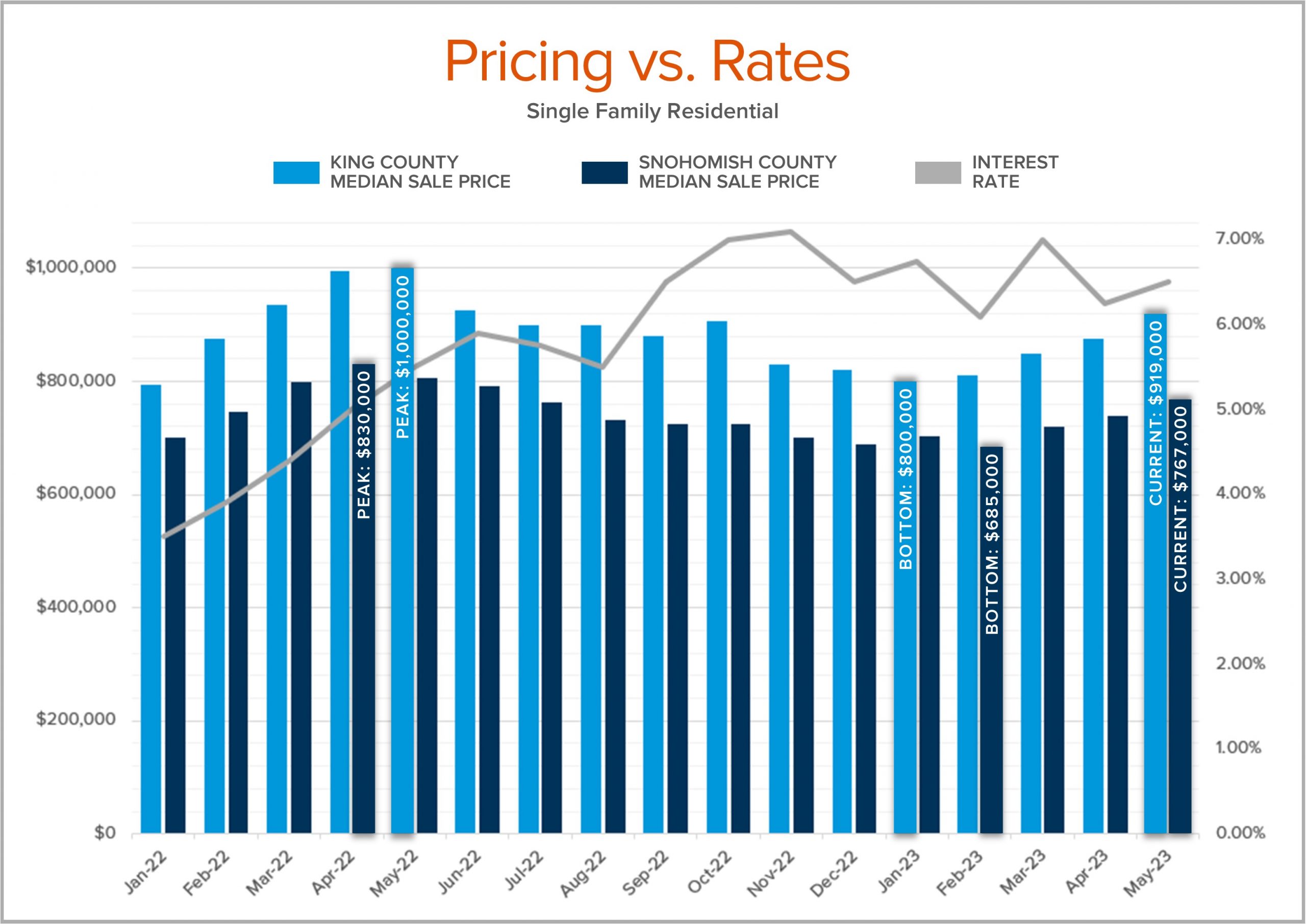

There has always been a direct correlation between interest rates and home prices. The rule of thumb has always been when rates go up prices go down, and vice versa. This was temporarily proven true in the summer of 2022 when rates quickly rose by 2% (3.5%-5.5%) over 5 months. It created a price correction in the second half of 2022 as buyers retreated from the market due to affordability. One should note that price acceleration was rapid from May 2020 to May 2022 and in that two-year period prices grew upward of 50% in King and Snohomish Counties. That was an unsustainable pace. In all honesty, this was inflation’s role in the housing market, and increasing the rates was the Fed’s way of getting control.

There has always been a direct correlation between interest rates and home prices. The rule of thumb has always been when rates go up prices go down, and vice versa. This was temporarily proven true in the summer of 2022 when rates quickly rose by 2% (3.5%-5.5%) over 5 months. It created a price correction in the second half of 2022 as buyers retreated from the market due to affordability. One should note that price acceleration was rapid from May 2020 to May 2022 and in that two-year period prices grew upward of 50% in King and Snohomish Counties. That was an unsustainable pace. In all honesty, this was inflation’s role in the housing market, and increasing the rates was the Fed’s way of getting control.

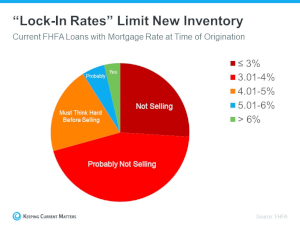

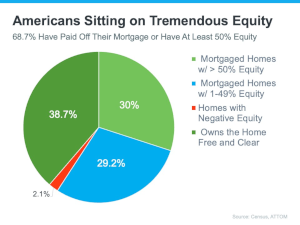

There are two interesting phenomena going on with potential home sellers right now. First, according to ATTOM Data, 68.7% of homeowners have at least 50% equity and only 2.1% have negative equity. This is the number one indicator that we are not in a housing crisis or bubble. Second, according to FHFA, 70% of homeowners with a mortgage have a rate 4% or lower. This is causing people who are no longer happy with where they live to stay a bit longer because they don’t want to give up their payment just yet.

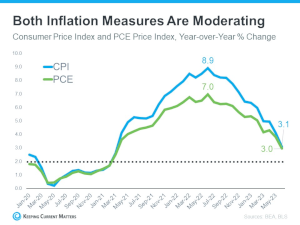

There are two interesting phenomena going on with potential home sellers right now. First, according to ATTOM Data, 68.7% of homeowners have at least 50% equity and only 2.1% have negative equity. This is the number one indicator that we are not in a housing crisis or bubble. Second, according to FHFA, 70% of homeowners with a mortgage have a rate 4% or lower. This is causing people who are no longer happy with where they live to stay a bit longer because they don’t want to give up their payment just yet. So, what is going to happen when rates come down? Experts across the board predict that rates will recede as inflation gains control. This will be a gradual process over the next 12-18 months. The biggest indicator will be inflation reaching the 2% year-over-year mark. Once we hit this point, which we are close to, experts predict the Fed will be comfortable easing off the higher rates. This will cause more homes to come to market as the delta between the rate a homeowner currently holds and what they are willing to take on to indulge their desire to move, will become more attainable. Plus, as rates recede it will increase buyer demand.

So, what is going to happen when rates come down? Experts across the board predict that rates will recede as inflation gains control. This will be a gradual process over the next 12-18 months. The biggest indicator will be inflation reaching the 2% year-over-year mark. Once we hit this point, which we are close to, experts predict the Fed will be comfortable easing off the higher rates. This will cause more homes to come to market as the delta between the rate a homeowner currently holds and what they are willing to take on to indulge their desire to move, will become more attainable. Plus, as rates recede it will increase buyer demand.

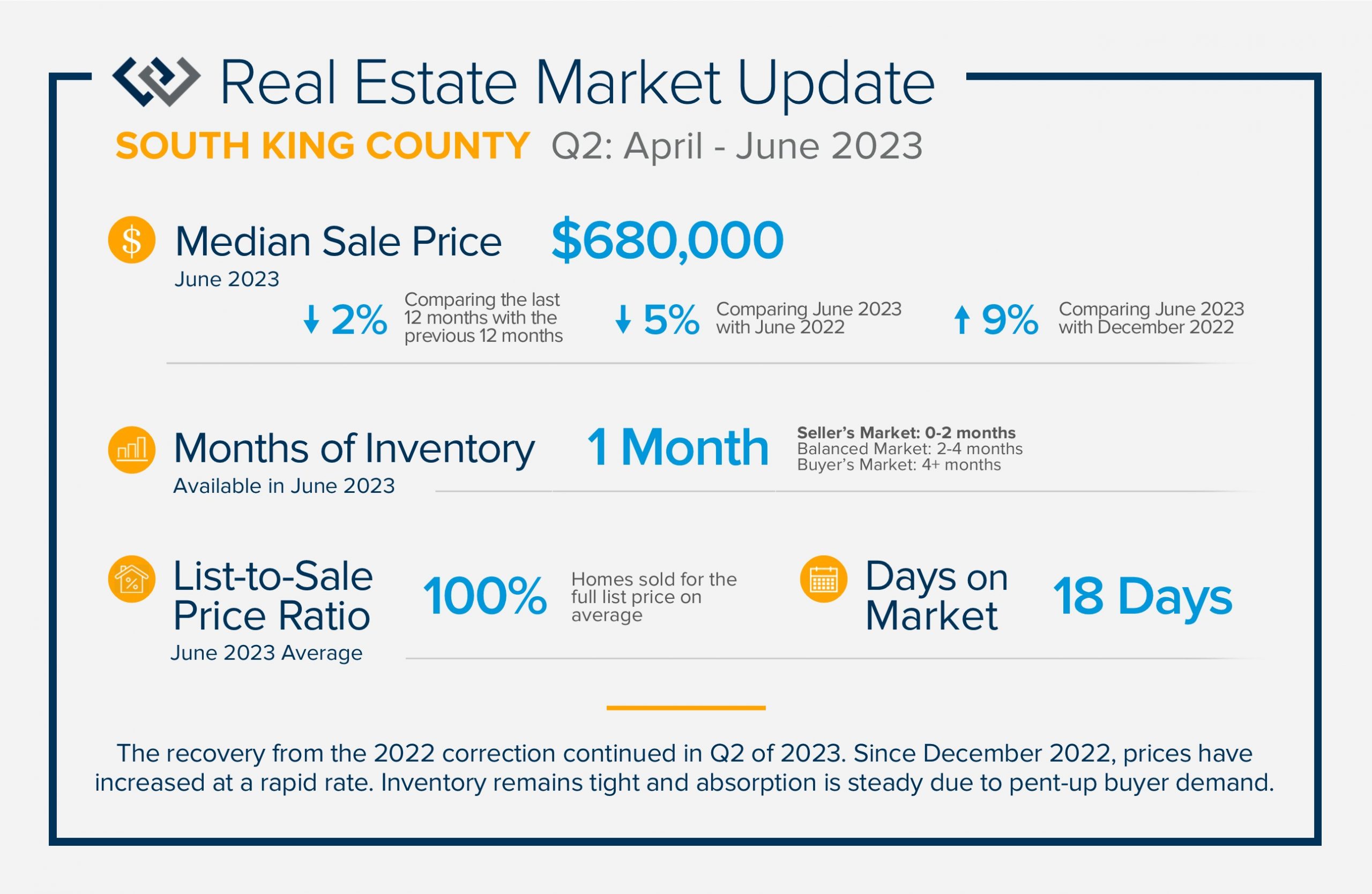

The recovery from the 2022 correction continued in Q2 of 2023. Since December 2022, prices have increased at a rapid rate. Inventory remains tight and absorption is steady due to pent-up buyer demand. Shorter days on market and healthy list-to-sale price ratios illustrate when a seller meets the market with appropriate pricing and is in good condition, a swift and successful sale is in store. Despite higher interest rates the market continues to churn. Rates are anticipated to come down, and when they do competition will increase.

The recovery from the 2022 correction continued in Q2 of 2023. Since December 2022, prices have increased at a rapid rate. Inventory remains tight and absorption is steady due to pent-up buyer demand. Shorter days on market and healthy list-to-sale price ratios illustrate when a seller meets the market with appropriate pricing and is in good condition, a swift and successful sale is in store. Despite higher interest rates the market continues to churn. Rates are anticipated to come down, and when they do competition will increase.

Windermere Community Service Day

Windermere Community Service Day

In King County, the median price peaked in May 2022 at $1M and is currently at $919,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in January 2023 at $800,000 which was down 20% (the actual tumble) from the peak but are now up 15% from the bottom!

In King County, the median price peaked in May 2022 at $1M and is currently at $919,000 (May 2023), which is down 8% from peak to current. Prices hit bottom in January 2023 at $800,000 which was down 20% (the actual tumble) from the peak but are now up 15% from the bottom!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

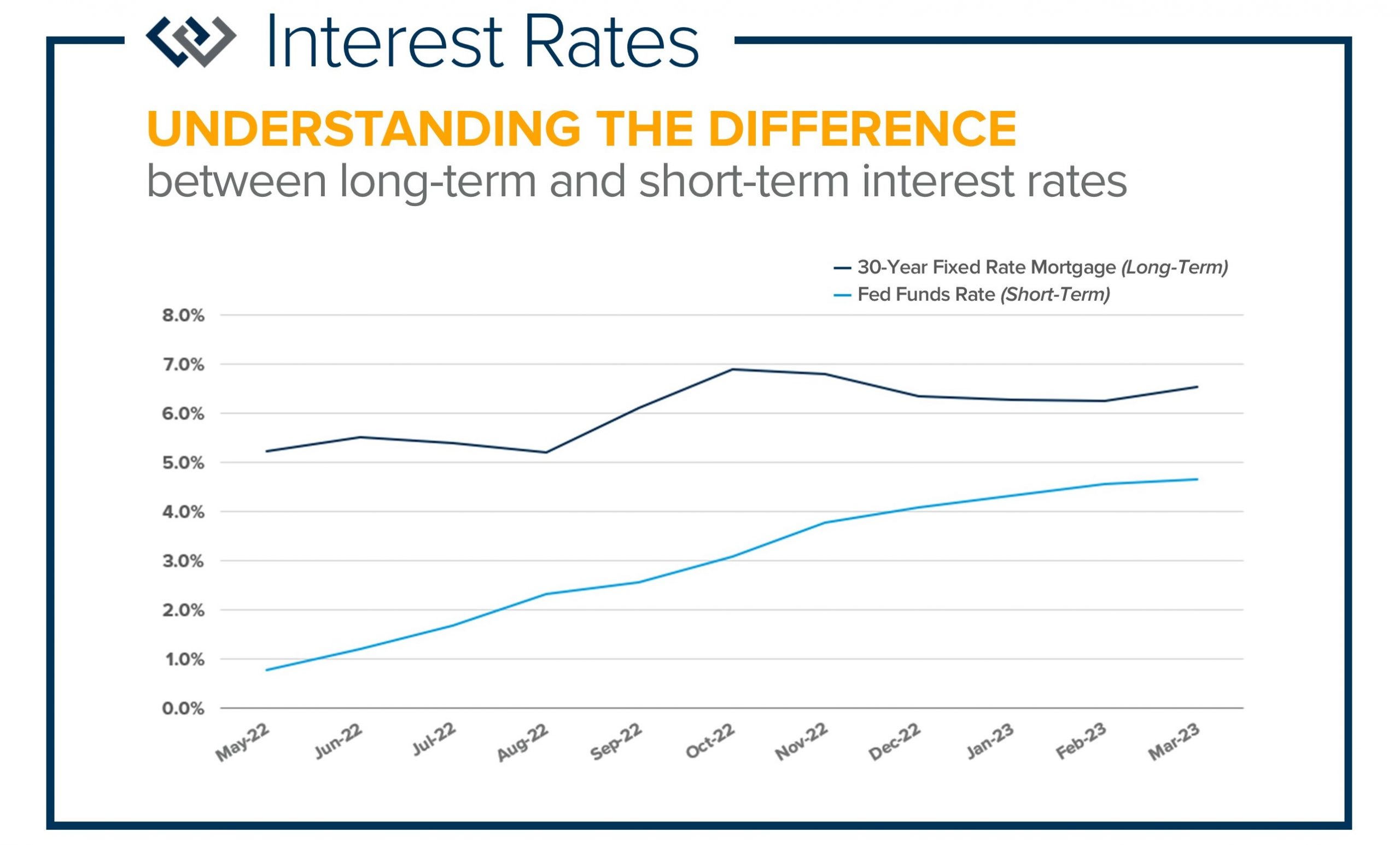

It is very important that consumers understand the difference between long-term interest rates and short-term interest rates. Long-term rates involve home mortgages such a conventional 30-year fixed, Jumbo, FHA, and VA loans. Short-term rates involve car loans, credit cards, and Home Equity Lines of Credit (HELOCs). While both types of rates have gone up over the course of the last year, they have not had the same trajectory.

It is very important that consumers understand the difference between long-term interest rates and short-term interest rates. Long-term rates involve home mortgages such a conventional 30-year fixed, Jumbo, FHA, and VA loans. Short-term rates involve car loans, credit cards, and Home Equity Lines of Credit (HELOCs). While both types of rates have gone up over the course of the last year, they have not had the same trajectory.

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

ATTENTION GARDENERS: Windermere Community Service Day is coming and we’d love your help!

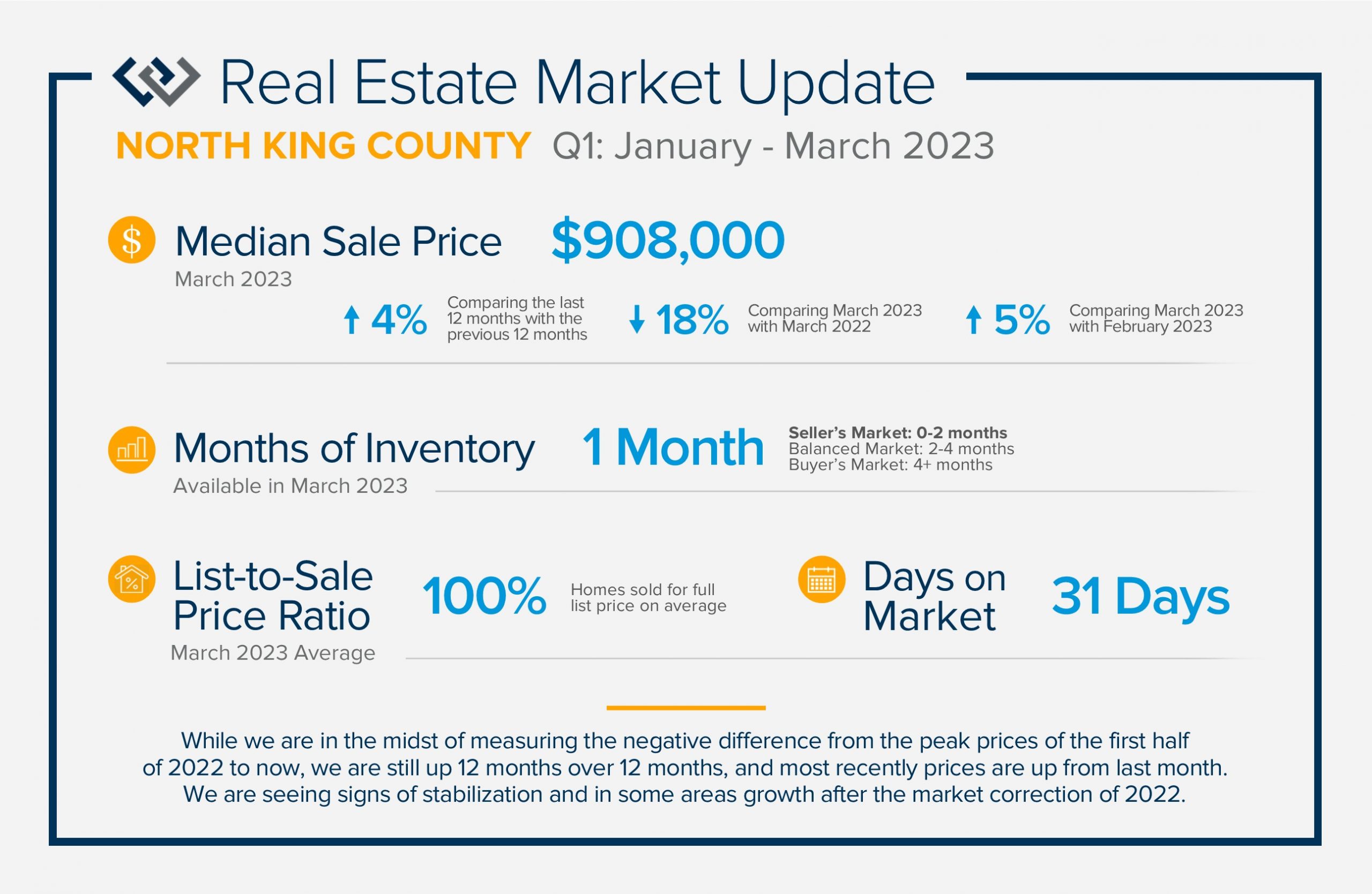

We are seeing signs of price stabilization and some growth after the market correction of 2022! Illustrated on the front is the up-down-up trajectory that home prices have experienced over the last year. While we are in the midst of measuring the negative difference from the peak prices of the first half of 2022 to now, we are still up 12 months over 12 months, and most recently prices are up from last month.

We are seeing signs of price stabilization and some growth after the market correction of 2022! Illustrated on the front is the up-down-up trajectory that home prices have experienced over the last year. While we are in the midst of measuring the negative difference from the peak prices of the first half of 2022 to now, we are still up 12 months over 12 months, and most recently prices are up from last month.

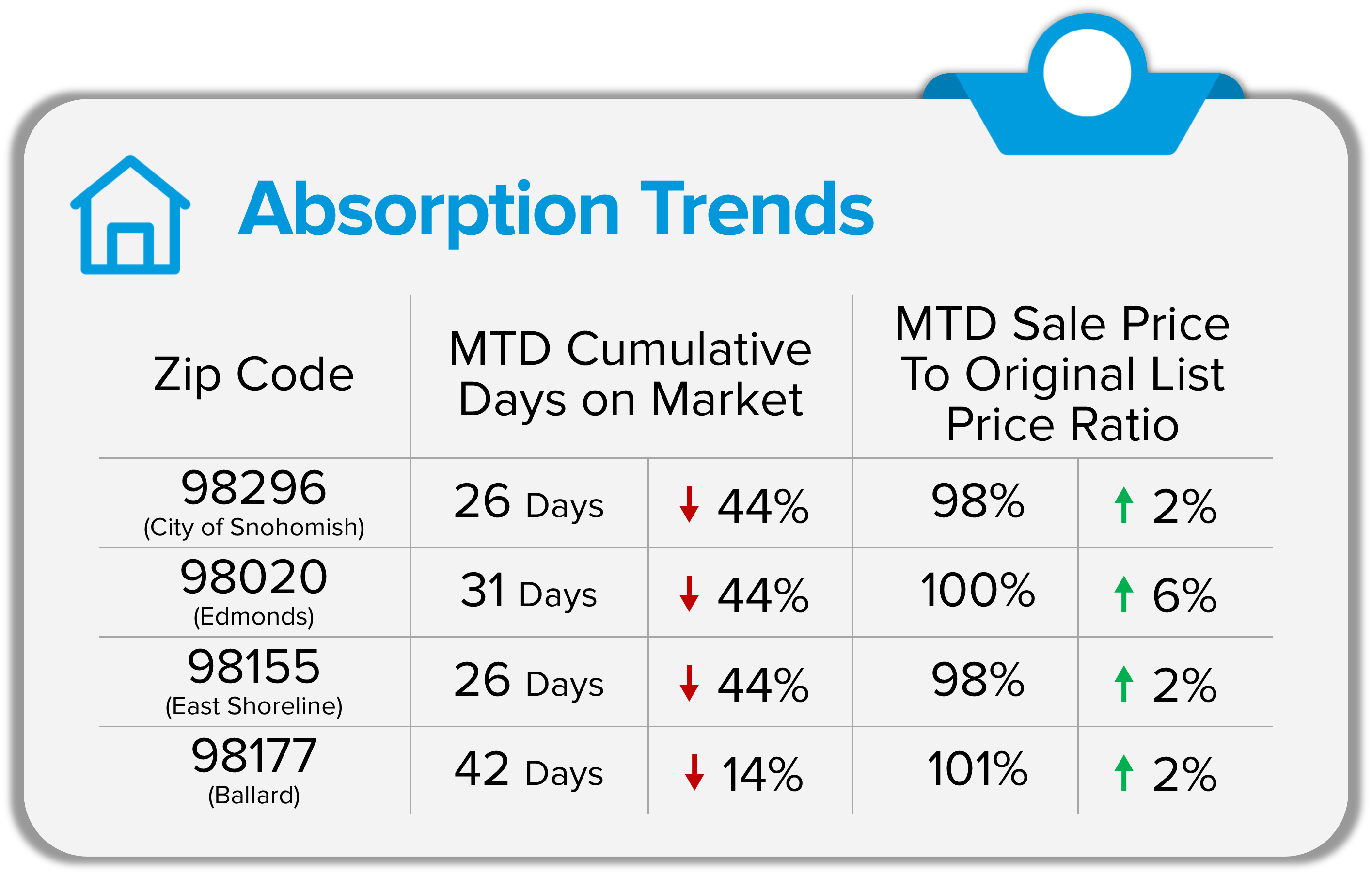

As we round out the first quarter of 2023, three real-time trends to pay close attention to in order to truly understand what is happening in the real estate market are absorption data, interest rates, and inventory levels. Right now, we are in the midst of the market heating up due to seasonality, pent-up buyer demand, and rates finding their new normal. The media will often lag in reporting the latest information (pending sale data) and will latch onto closed sale data, which is outdated. I am here to keep you on the frontline of market activity so you are connected to the most current data to keep you well informed.

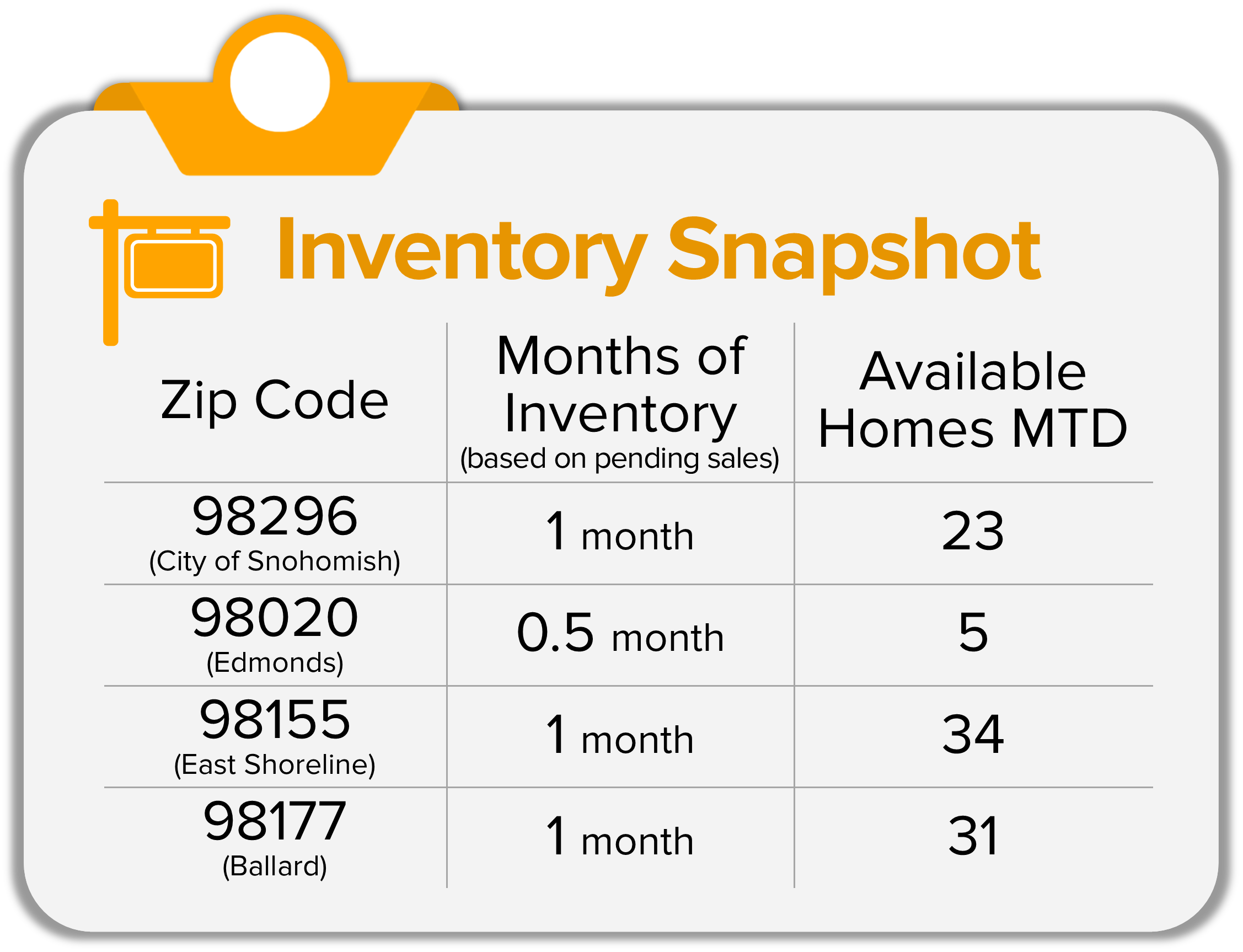

As we round out the first quarter of 2023, three real-time trends to pay close attention to in order to truly understand what is happening in the real estate market are absorption data, interest rates, and inventory levels. Right now, we are in the midst of the market heating up due to seasonality, pent-up buyer demand, and rates finding their new normal. The media will often lag in reporting the latest information (pending sale data) and will latch onto closed sale data, which is outdated. I am here to keep you on the frontline of market activity so you are connected to the most current data to keep you well informed. Available inventory is constricting due to an increase in absorption and new listings lagging. As we head into spring, we will see a seasonal uptick in new listings which will be welcomed by a healthy buyer audience. Month-to-date, inventory levels based on pending sales show a seller’s market (0-2 months). You calculate months of inventory by taking the number of available homes and dividing it by the number of pending sales. If no new homes came to market the trend suggests we would sell out of homes in this amount of time. Month-to-date the actual number of homes available in each zip code is quite limited and a welcome sign for more new listings as we head into Spring. Again, I pulled the data for the four zip codes to represent a sampling of both Snohomish and King Counties.

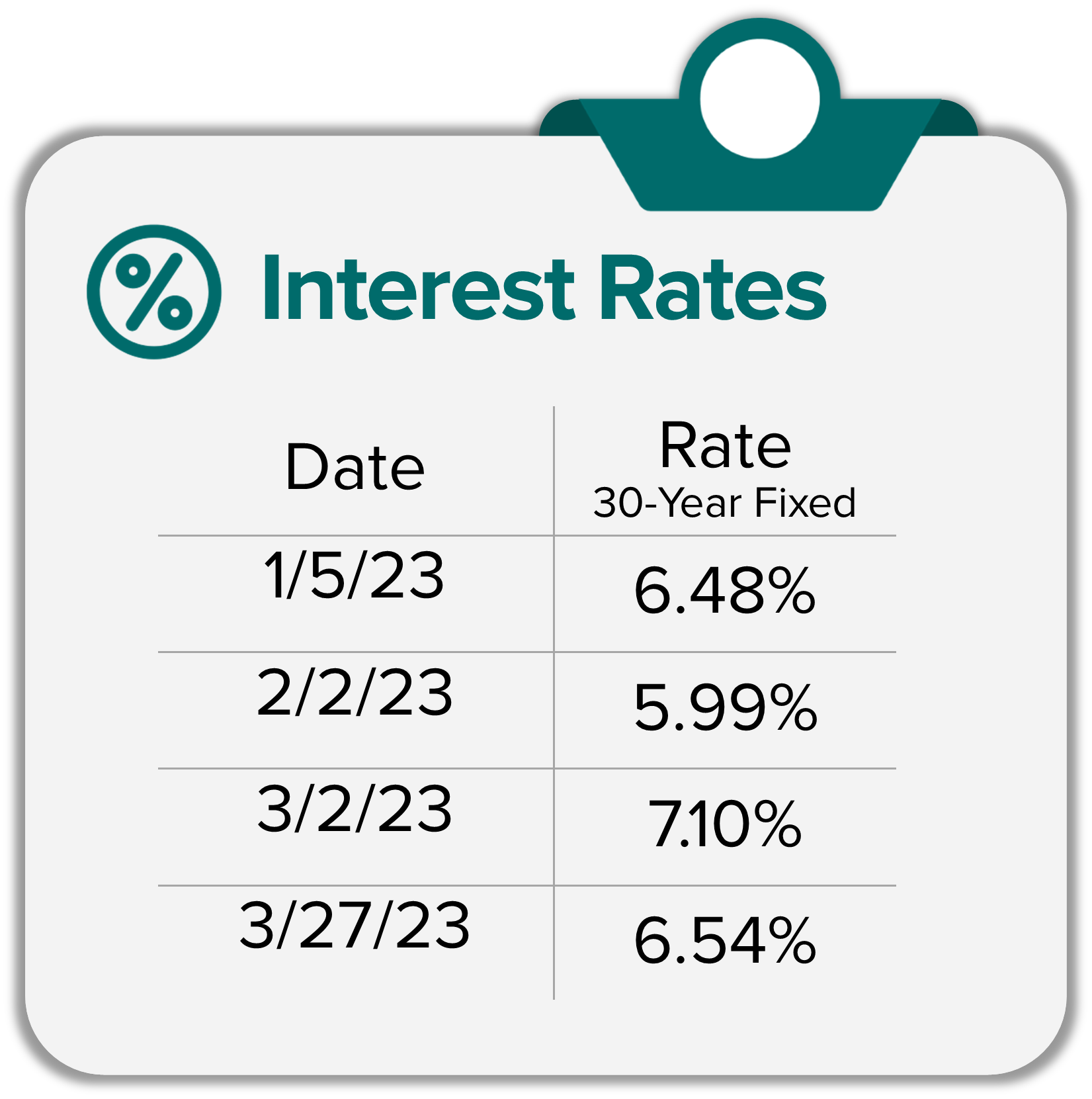

Available inventory is constricting due to an increase in absorption and new listings lagging. As we head into spring, we will see a seasonal uptick in new listings which will be welcomed by a healthy buyer audience. Month-to-date, inventory levels based on pending sales show a seller’s market (0-2 months). You calculate months of inventory by taking the number of available homes and dividing it by the number of pending sales. If no new homes came to market the trend suggests we would sell out of homes in this amount of time. Month-to-date the actual number of homes available in each zip code is quite limited and a welcome sign for more new listings as we head into Spring. Again, I pulled the data for the four zip codes to represent a sampling of both Snohomish and King Counties. At the start of 2023, the 30-year fixed mortgage was at 6.48%, then dropped to 5.99% in early February, peaked at 7.1% in early March, and is now back down to 6.54% at press time. Rates have been volatile as the Fed tries to manage inflation. You can access a video below from

At the start of 2023, the 30-year fixed mortgage was at 6.48%, then dropped to 5.99% in early February, peaked at 7.1% in early March, and is now back down to 6.54% at press time. Rates have been volatile as the Fed tries to manage inflation. You can access a video below from  During this time of change, it is important that each neighborhood and price point is researched individually. From the four zip code breakdowns above, it is clear that the trends vary. When I am asked the question, “How’s the Market?”, I am always curious to know what you have heard and what you want to learn about. Sweeping statements are dangerous and I am committed to diving into the data to educate my clients on how the trends affect their investments and their lifestyle.

During this time of change, it is important that each neighborhood and price point is researched individually. From the four zip code breakdowns above, it is clear that the trends vary. When I am asked the question, “How’s the Market?”, I am always curious to know what you have heard and what you want to learn about. Sweeping statements are dangerous and I am committed to diving into the data to educate my clients on how the trends affect their investments and their lifestyle.

You’re invited to our annual Paper Shredding Event & Food Drive. We partner with

You’re invited to our annual Paper Shredding Event & Food Drive. We partner with