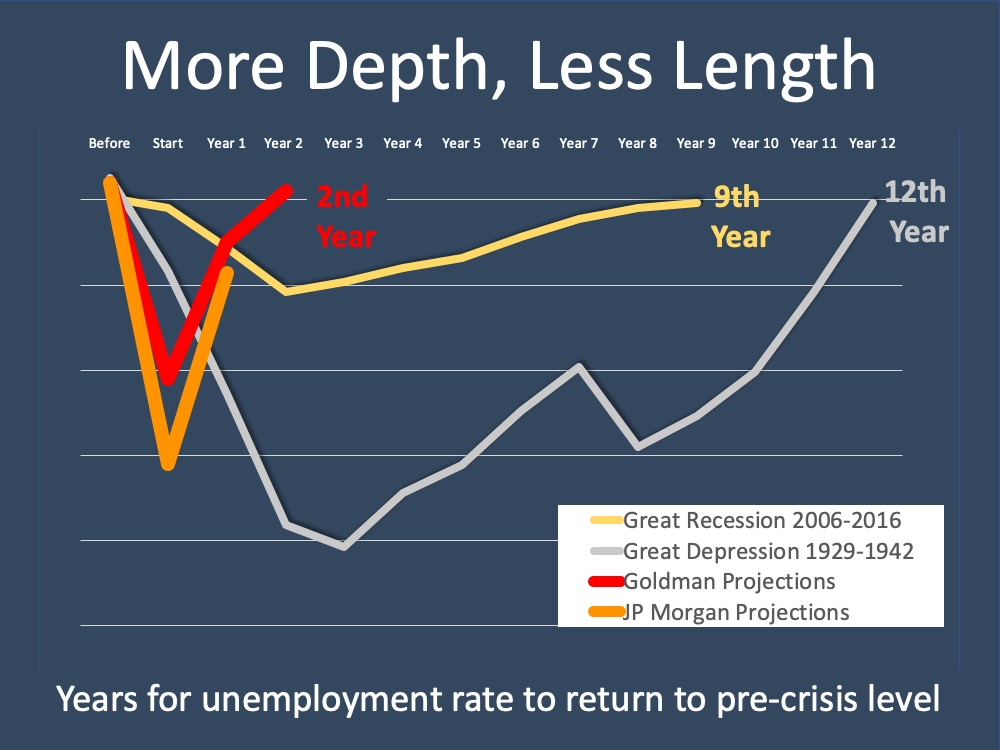

Are we Headed Towards a Repeat of the 2008 Housing Meltdown?

The pressure the COVID-19 global pandemic is putting on the economy is a reality. As a real estate broker, I take great pride in having the honor of being your trusted advisor when it comes to your investment in the housing market and protecting the value of your home. I have been asked several times, “Is this the Great Recession all over again?”

At Windermere, we have continued to rely on the expertise of Matthew Gardner, Windermere’s Chief Economist. Above is a chart he shared from Black Knight Financial comparing the housing market as we headed into this global health crisis versus the start of the Great Recession in 2007. Below is an 11-minute video going over the chart line by line. I urge you to watch the video and key in to his expertise versus what you might hear in the media. Matthew predicted the Great Recession and does not shy away from heeding the truth, even if it is not great news. I trust him and I hope you do too.

Bottom line, we are heading into this economic challenge with a much more formidable foundation based on more stringent lending practices, higher equity levels, and we are anticipating a shorter 1-2 year V-shaped recovery, compared to the long U-shaped recovery of the 5-year Great Recession. In fact, we have seen pending sales rise over the last three consecutive weeks, some even with multiple offers. Every neighborhood and every price-point has its own story. Please reach out with any questions or concerns. It is my goal to help keep you informed and empower strong decisions.

We’re on a mission to help our local food banks keep their shelves stocked during this uncertain time. For every dollar our office raises, the Windermere Foundation is matching up to $3,500 through May 5th! This is a part of a total of $250,000 in matching funds from the Windermere Foundation, with the goal to give $500,000 to food banks across the areas that Windermere serves.

The need has never been greater, so we’re partnering with the trusted Volunteers of America (VOA) of Snohomish County, who know how to stretch every dollar to its fullest extent and successfully manage many of the food banks and food pantries across the county. In addition, a portion of the total raised will go towards buying vegetable starts for the Martha Perry Veggie Garden (MPVG) managed by the Snohomish Garden Club (SGC) – which will supply local food banks withthousands of pounds of fresh produce throughout the summer and early fall.

Our team of agents at Windermere North will be planting close to an acre of starts on behalf of the VOA at the MPVG with the SGC the end of May into early June in small groups practicing proper social distancing. We have done this project for three years as a larger group and we are thrilled to creatively get it done this year. Food Banks have always coveted fresh produce and this effort will be more meaningful than ever this year.

If you are able to give, any amount will help make an impact and directly benefit our Neighbors in Need: gf.me/u/xy7ikd

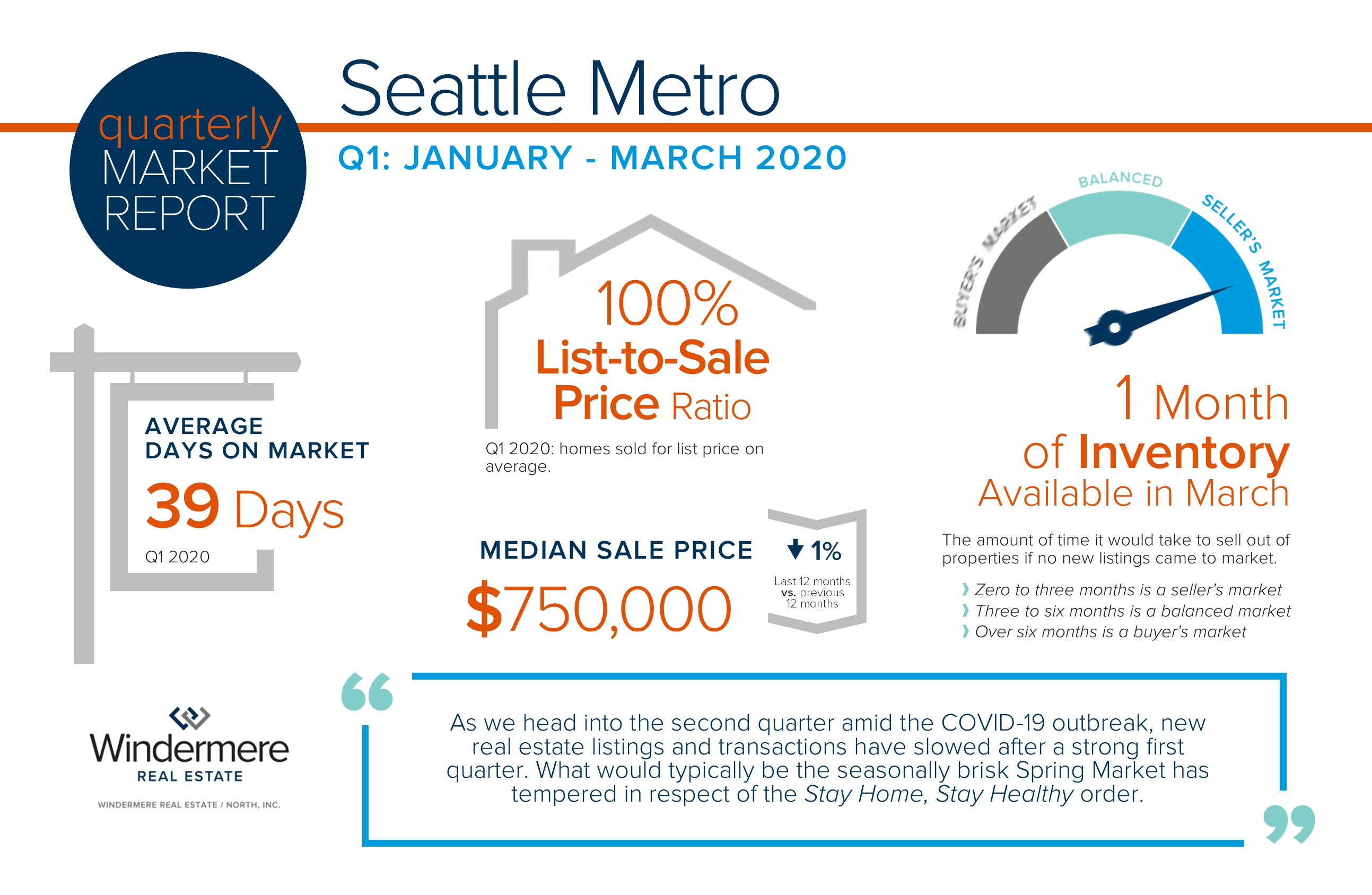

As we head into the second quarter amid the COVID-19 outbreak, new real estate listings and transactions have slowed after a strong first quarter. What would typically be the seasonally brisk Spring Market has tempered in respect of the Stay Home, Stay Healthy order.

During this time, some sellers are still coming to market and there are motivated buyers carefully viewing and purchasing homes. I’m happy to report that sellers are maintaining their home sale values through these negotiations. We anticipate pent-up demand for both sellers and buyers once the orders are lifted, and see the summer season becoming the new spring for real estate and a more normal second half of 2020, bearing control of the virus. We also look forward to many jobs returning once the orders are lifted. We are fortunate to be in the Greater Seattle Area, as many industries such as tech and biotech will hold small businesses on their shoulders once their workers return to the brick and mortar locations.

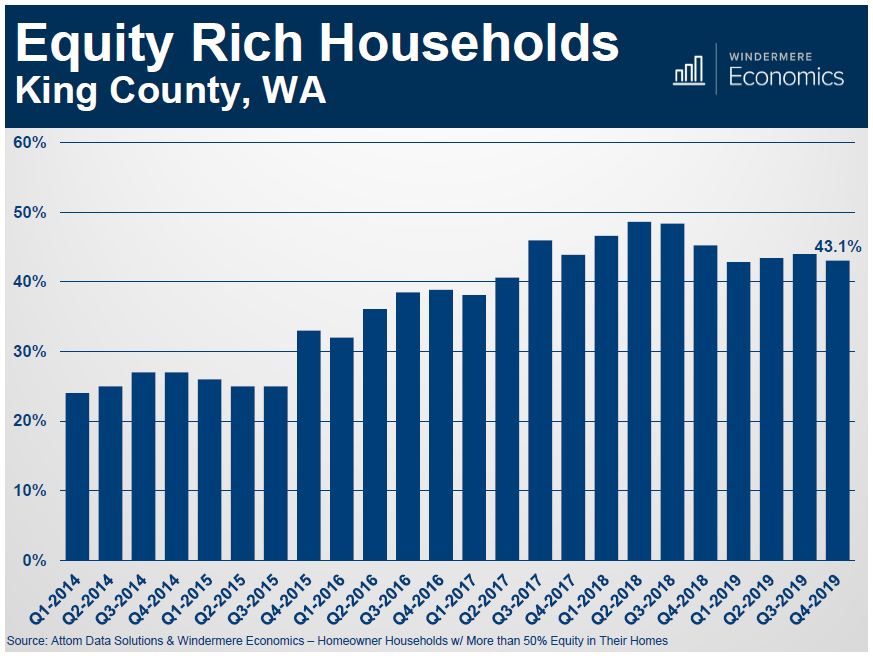

Prior to the outbreak, we anticipated complete year-over-year price growth to be 4-6%. That has been adjusted to 1-3% due to this health crisis. Another important element to consider is equity levels: 43% of homeowners in King County have more than 50% equity in their home.

These are unprecedented times and there are many questions and concerns. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

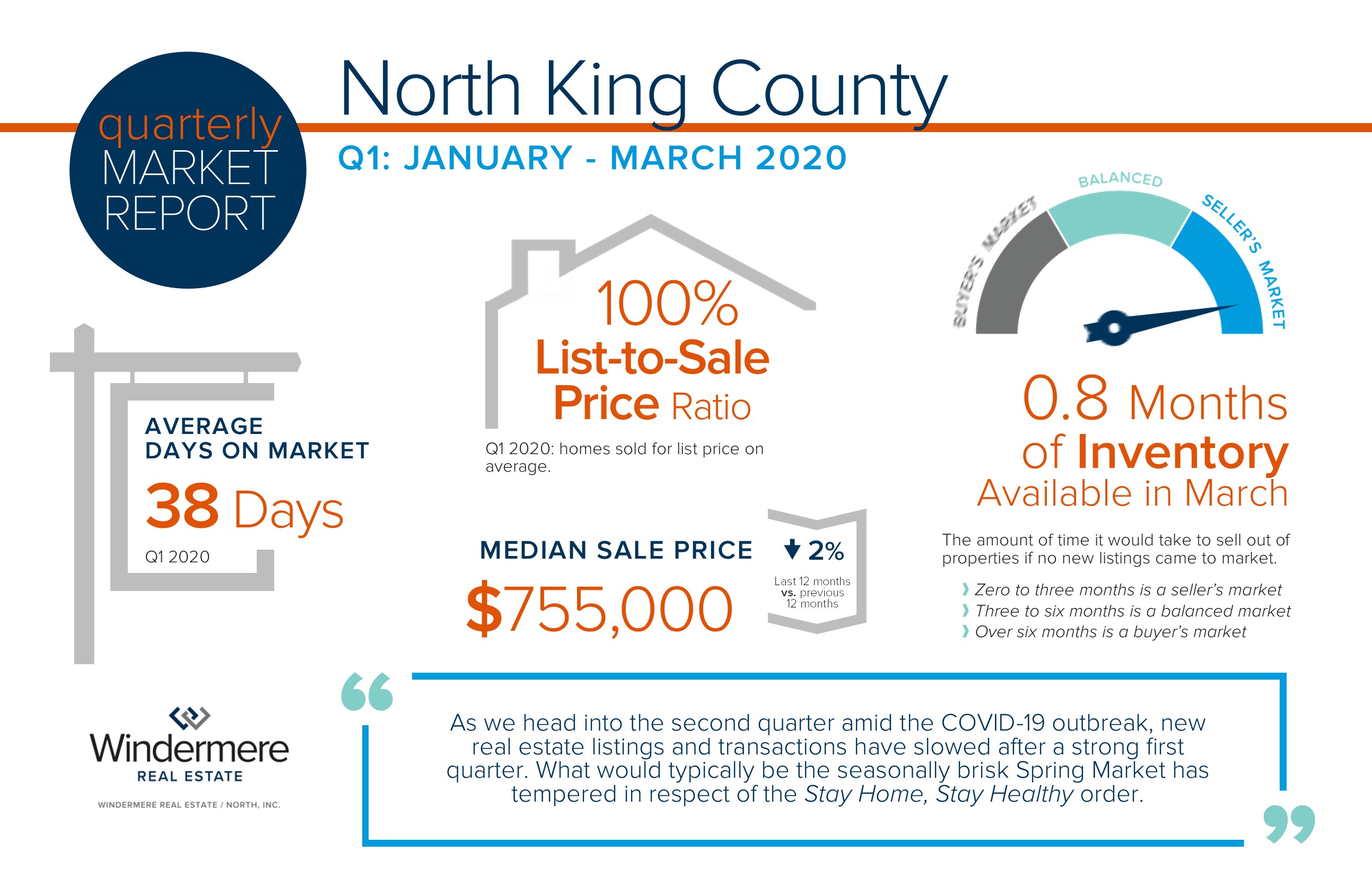

As we head into the second quarter amid the COVID-19 outbreak, new real estate listings and transactions have slowed after a strong first quarter. What would typically be the seasonally brisk Spring Market has tempered in respect of the Stay Home, Stay Healthy order.

During this time, some sellers are still coming to market and there are motivated buyers carefully viewing and purchasing homes. I’m happy to report that sellers are maintaining their home sale values through these negotiations. We anticipate pent-up demand for both sellers and buyers once the orders are lifted, and see the summer season becoming the new spring for real estate and a more normal second half of 2020, bearing control of the virus. We also look forward to many jobs returning once the orders are lifted. We are fortunate to be in the Greater Seattle Area, as many industries such as tech and biotech will hold small businesses on their shoulders once their workers return to the brick and mortar locations.

Prior to the outbreak, we anticipated complete year-over-year price growth to be 4-6%. That has been adjusted to 1-3% due to this health crisis. Another important element to consider is equity levels: 43% of homeowners in King County have more than 50% equity in their home.

These are unprecedented times and there are many questions and concerns. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

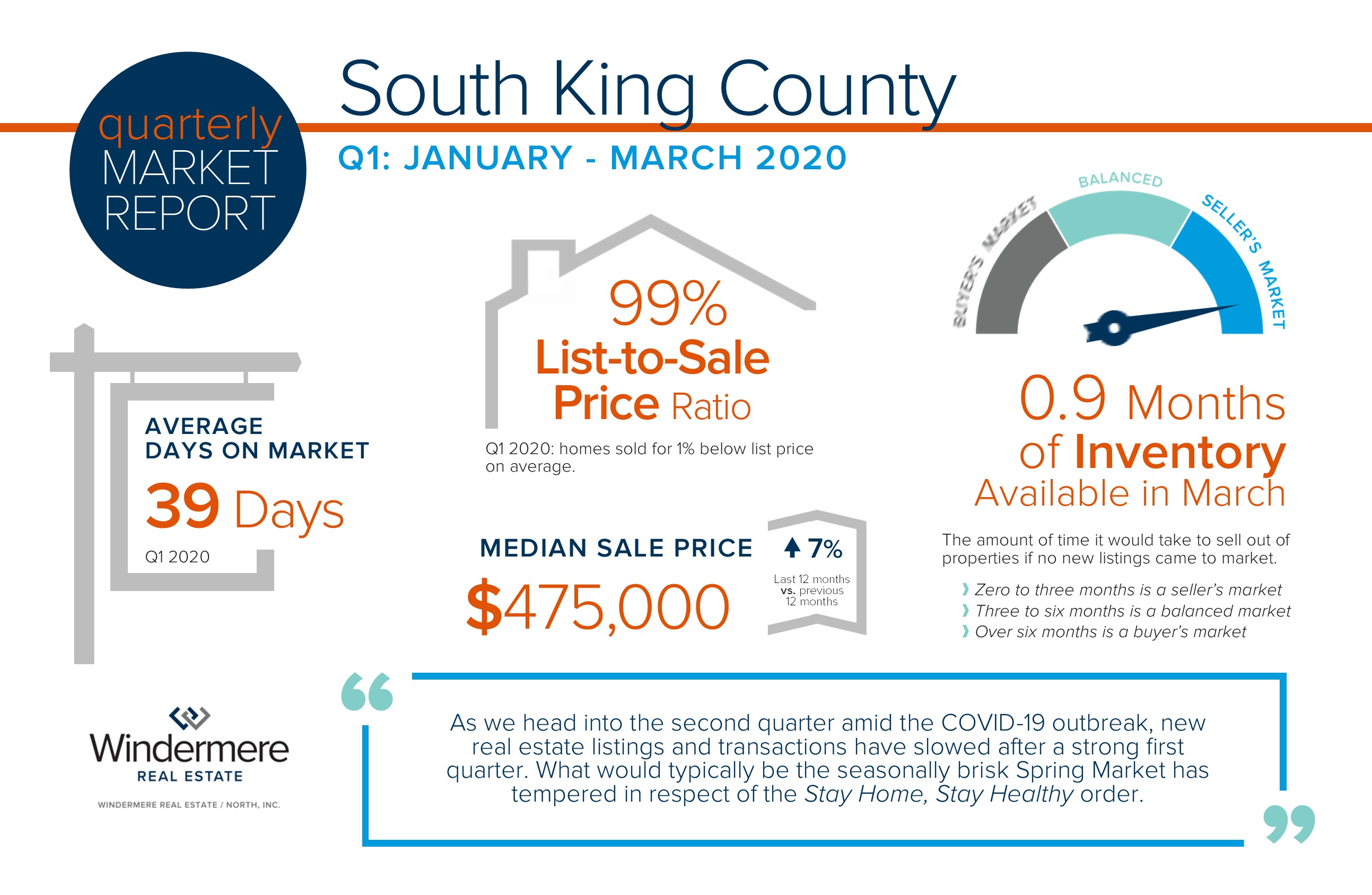

As we head into the second quarter amid the COVID-19 outbreak, new real estate listings and transactions have slowed after a strong first quarter. What would typically be the seasonally brisk Spring Market has tempered in respect of the Stay Home, Stay Healthy order.

During this time, some sellers are still coming to market and there are motivated buyers carefully viewing and purchasing homes. I’m happy to report that sellers are maintaining their home sale values through these negotiations. We anticipate pent-up demand for both sellers and buyers once the orders are lifted, and see the summer season becoming the new spring for real estate and a more normal second half of 2020, bearing control of the virus. We also look forward to many jobs returning once the orders are lifted. We are fortunate to be in the Greater Seattle Area, as many industries such as tech and biotech will hold small businesses on their shoulders once their workers return to the brick and mortar locations.

Prior to the outbreak, we anticipated complete year-over-year price growth to be 4-6%. That has been adjusted to 1-3% due to this health crisis. Another important element to consider is equity levels: 43% of homeowners in King County have more than 50% equity in their home.

These are unprecedented times and there are many questions and concerns. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

As we head into the second quarter amid the COVID-19 outbreak, new real estate listings and transactions have slowed after a strong first quarter. What would typically be the seasonally brisk Spring Market has tempered in respect of the Stay Home, Stay Healthy order.

During this time, some sellers are still coming to market and there are motivated buyers carefully viewing and purchasing homes. I’m happy to report that sellers are maintaining their home sale values through these negotiations. We anticipate pent-up demand for both sellers and buyers once the orders are lifted, and see the summer season becoming the new spring for real estate and a more normal second half of 2020, bearing control of the virus. We also look forward to many jobs returning once the orders are lifted. We are fortunate to be in the Greater Seattle Area, as many industries such as tech and biotech will hold small businesses on their shoulders once their workers return to the brick and mortar locations.

Prior to the outbreak, we anticipated complete year-over-year price growth to be 4-6%. That has been adjusted to 1-3% due to this health crisis. Another important element to consider is equity levels: 43% of homeowners in King County have more than 50% equity in their home.

These are unprecedented times and there are many questions and concerns. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

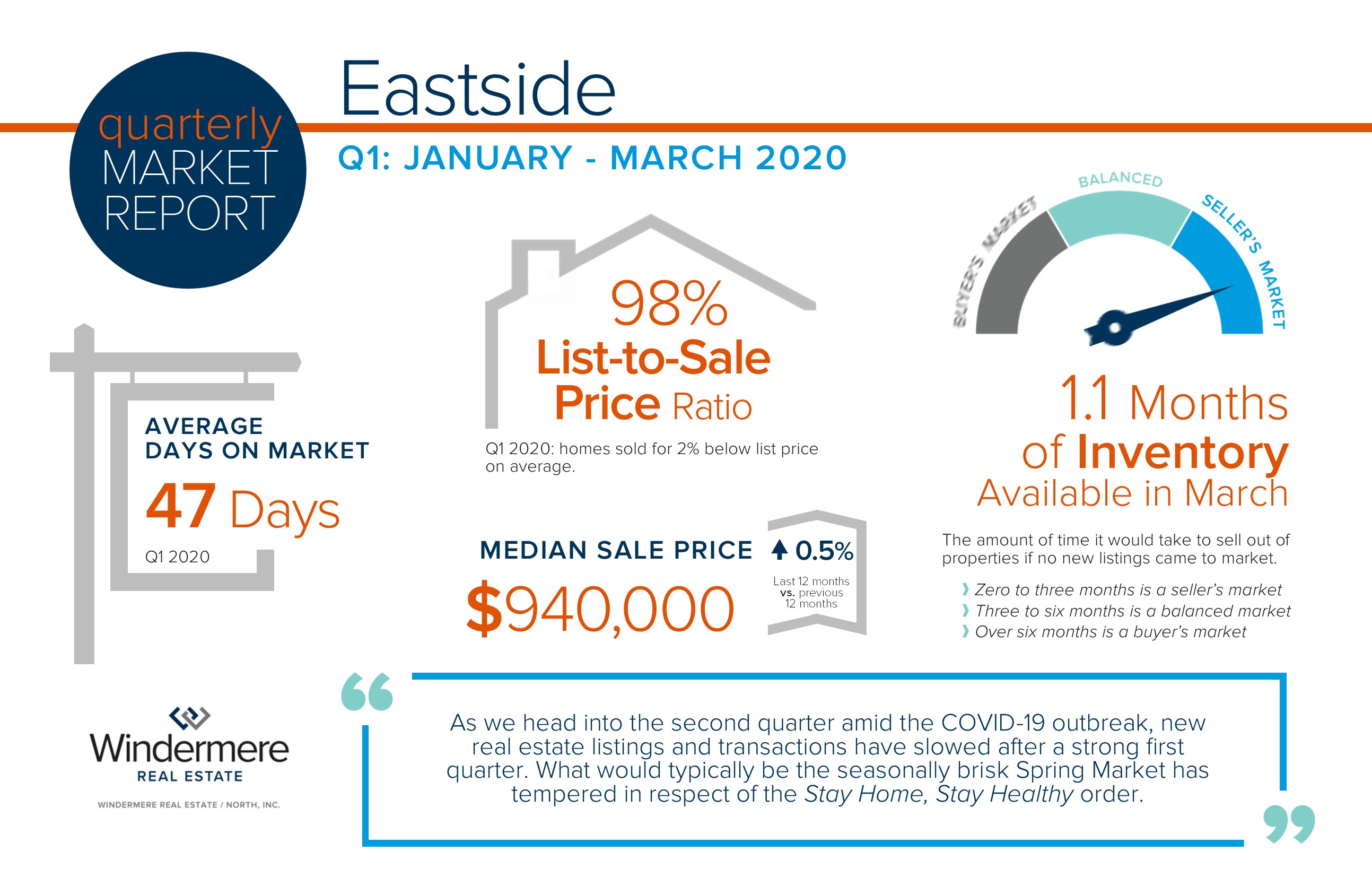

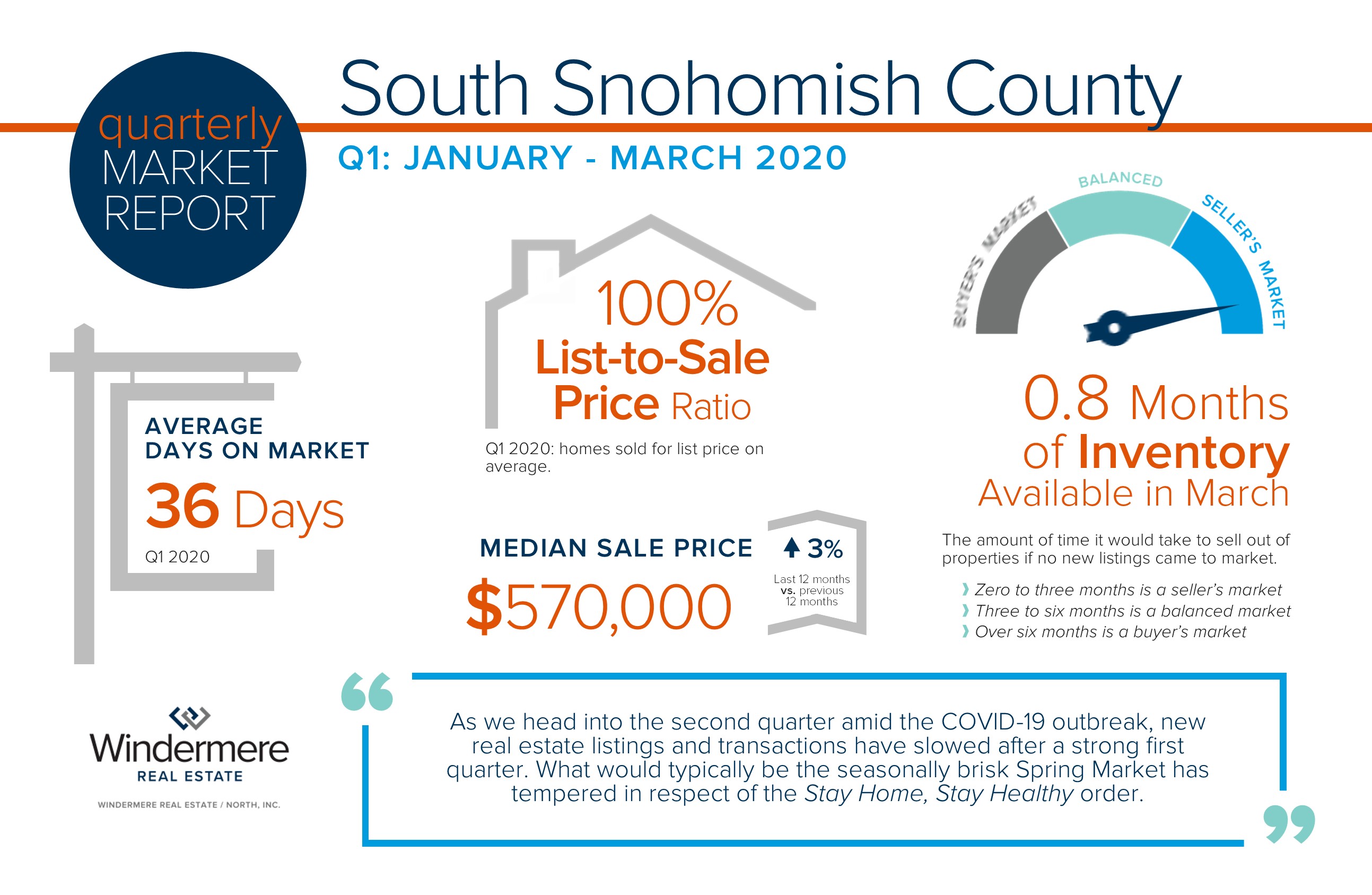

As we head into the second quarter amid the COVID-19 outbreak, new real estate listings and transactions have slowed after a strong first quarter. What would typically be the seasonally brisk Spring Market has tempered in respect of the Stay Home, Stay Healthy order.

During this time, some sellers are still coming to market and there are motivated buyers carefully viewing and purchasing homes. I’m happy to report that sellers are maintaining their home sale values through these negotiations. We anticipate pent-up demand for both sellers and buyers once the orders are lifted, and see the summer season becoming the new spring for real estate and a more normal second half of 2020, bearing control of the virus. We also look forward to many jobs returning once the orders are lifted. We are fortunate to be in the Greater Seattle Area, as many industries such as tech and biotech will hold small businesses on their shoulders once their workers return to the brick and mortar locations.

Prior to the outbreak, we anticipated complete year-over-year price growth to be 4-6%. That has been adjusted to 1-3% due to this health crisis. Another important element to consider is equity levels: 33% of homeowners in Snohomish County have more than 50% equity in their home.

These are unprecedented times and there are many questions and concerns. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

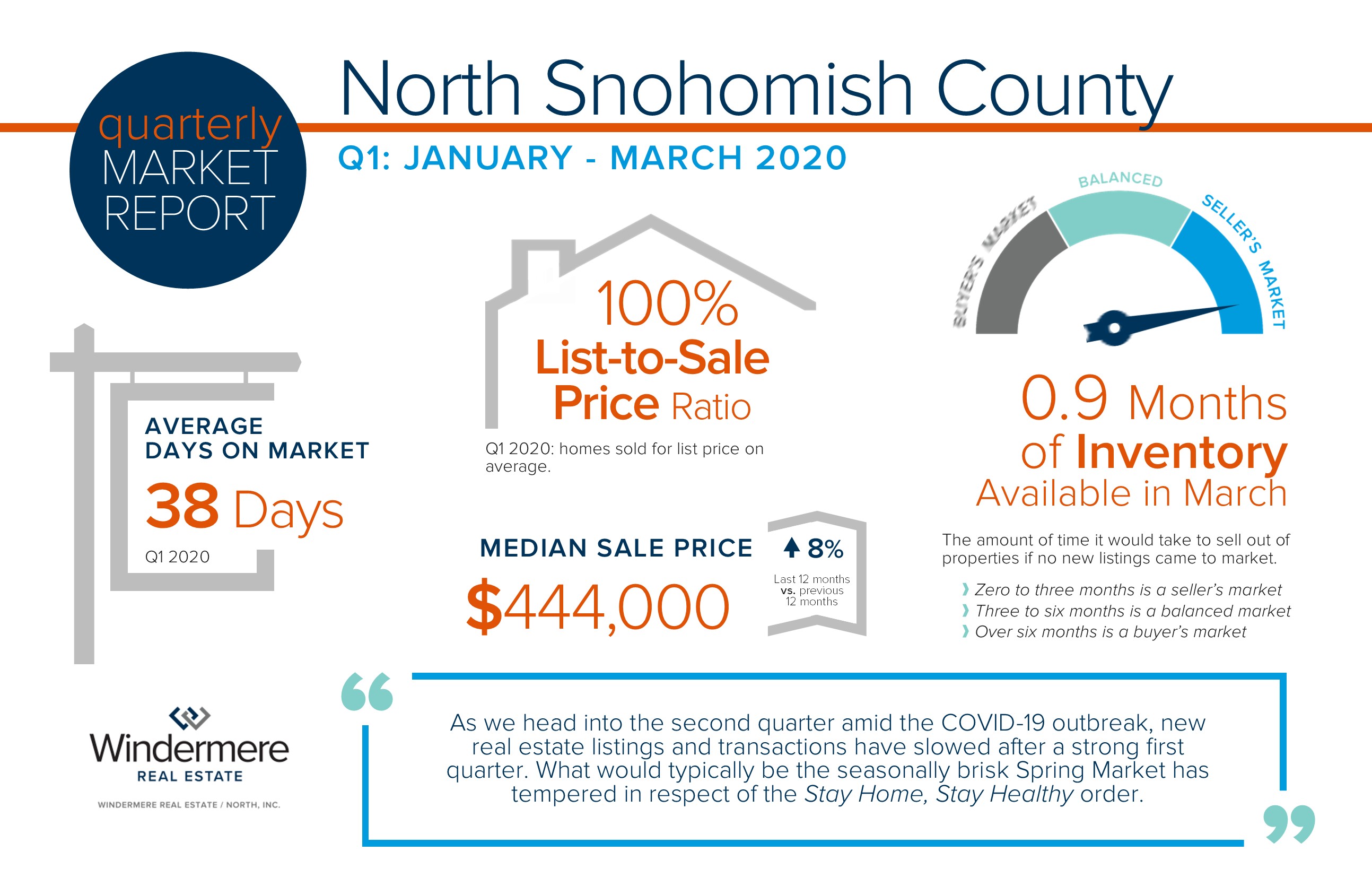

As we head into the second quarter amid the COVID-19 outbreak, new real estate listings and transactions have slowed after a strong first quarter. What would typically be the seasonally brisk Spring Market has tempered in respect of the Stay Home, Stay Healthy order.

During this time, some sellers are still coming to market and there are motivated buyers carefully viewing and purchasing homes. I’m happy to report that sellers are maintaining their home sale values through these negotiations. We anticipate pent-up demand for both sellers and buyers once the orders are lifted, and see the summer season becoming the new spring for real estate and a more normal second half of 2020, bearing control of the virus. We also look forward to many jobs returning once the orders are lifted. We are fortunate to be in the Greater Seattle Area, as many industries such as tech and biotech will hold small businesses on their shoulders once their workers return to the brick and mortar locations.

Prior to the outbreak, we anticipated complete year-over-year price growth to be 4-6%. That has been adjusted to 1-3% due to this health crisis. Another important element to consider is equity levels: 33% of homeowners in Snohomish County have more than 50% equity in their home.

These are unprecedented times and there are many questions and concerns. It is my goal to help keep my clients informed and empower strong decisions, now more than ever. Please reach out if you’d like to discuss your real estate goals and how they relate to your lifestyle and bottom line. Be well!

Due to the Stay Home, Stay Healthy orders being extended through May 4th, our annual Shred Event & Food Drive has been postponed to July 18, the first Saturday after the new income tax filing deadline. The safety of the attendees, our agents, staff and the public at large is our highest priority. We sincerely apologize for any inconvenience this may cause and look forward to seeing you in July!

This is our 9th year partnering with Confidential Data Disposal; providing you with a safe, eco-friendly way to reduce your paper trail and help prevent identity theft.

Saturday, July 18th, 10AM to 2PM

4211 Alderwood Mall Blvd, Lynnwood.

Bring your sensitive documents to be professionally destroyed on-site. Limit 20 file boxes per visitor.

We will also be collecting non-perishable food and cash donations to benefit Concern for Neighbors food bank. Donations are not required, but are appreciated.

**This is a Paper-Only event. No x-rays, electronics, recyclables, or any other materials.

As we head into week four of the Stay Home/Stay Healthy orders in Washington State, I turn my thoughts towards my gratitude for housing. It’s safe to say that over the last few weeks we’ve become quite intimate with our four walls, the brick and mortar that we call home. Concrete, steel, wood, and glass make up the structure that keeps us safe and protected, but it’s who and what is inside that makes it a home.

I don’t know about you, but I’ve never spent so much time in my home. This has developed a greater appreciation of the little things that make it special and even an acceptance of my not-so-favorite features. That quiet corner I can sneak away to, a blooming spring garden, a functional kitchen to create meals, and the community that surrounds us during a time of isolation are just a few items on my list of thank-yous. Our homes have become our sanctuaries, now more than ever. It goes beyond the sticks and stones that hold it upright; it is the heart in which our lives are pulsing.

I’ve always taken my role in helping people with their housing very seriously. To be asked to assist people in the purchase or sale of their home is an honor. The careful steps taken to protect liabilities and keen negotiations to ensure the highest and best value are very important components and ones I have a passion for. Now though, envisioning the connection one has or could have with a home is seen more deeply.

It is customary to have a list of features that one desires in a home and to pursue those features in the hunt for new housing or to celebrate them when selling. Buying and selling real estate is an emotional process and this experience has highlighted that connection more than I’ve ever realized before. Navigating finances is sensitive, but getting to the core of where you will spend your days or say good-bye to the place that housed you is meaningful. I’ve always seen real estate as a relationship business; while we do transactions that have a beginning and an end, the relationships are ongoing beyond the closing of a sale.

I wanted to take this time to say thank you for allowing me to be your trusted advisor when it comes to your housing. It means a lot to be a part of something so special and important in people’s lives. Also, just a reminder to please use me as a resource if you need any help maintaining your home. I have a list of reputable contractors and service providers that can help you care for your home should you have something break or want to make an improvement.

We’ve never navigated an environment like this before and I am committed to helping you stay informed. I’m happy to report that we are still seeing positive real estate activity happening during the Stay Home/Stay Healthy orders. My next newsletter, in two weeks will re-cap the latest statistics and will start to tell the more complete story of COVID-19 and real estate. We headed into this health crisis on the shoulders of a very strong first quarter in real estate and still have many positive economic influences in the PNW. I am certain there will be pent up demand on the other side of this historical time and I am hopeful many jobs will return. Stay tuned for this upcoming report and please reach out if you’d like to discuss now. In the meantime, I wish you and yours good health, a warm heart, and a happy home. Be well!

I hope this newsletter finds you and yours feeling well and making the best of the Stay Home, Stay Healthy order. It has been my goal as we navigate the COVID-19 pandemic to help keep my clients informed on how this is affecting real estate. I have received many inquiries asking about how the real estate market in our area is faring during this time. Fortunately, I have access to Matthew Gardner, Windermere’s Chief Economist on a weekly basis. Matthew’s one of the most respected economists in the nation, specifically in relation to housing. Last week, I had the opportunity to sit in on a Zoom meeting with him and my colleagues to learn more about COVID-19 and the Western Washington real estate market, and I found his outlook reassuring. Below is the latest edition of a weekly video series that he is recording each Monday to help keep everyone informed and connected to meaningful data. Matthew Gardner and Steve Harney, another economist on the East Coast, are who I am looking to for answers in contrast to just turning on the news or reading the latest headlines. Please click on the image below to listen to Matthew. If you have any questions or want to discuss how this might affect your real estate position specifically, please reach out! It has always been my goal to help keep my clients informed and empower strong decisions, now more than ever.

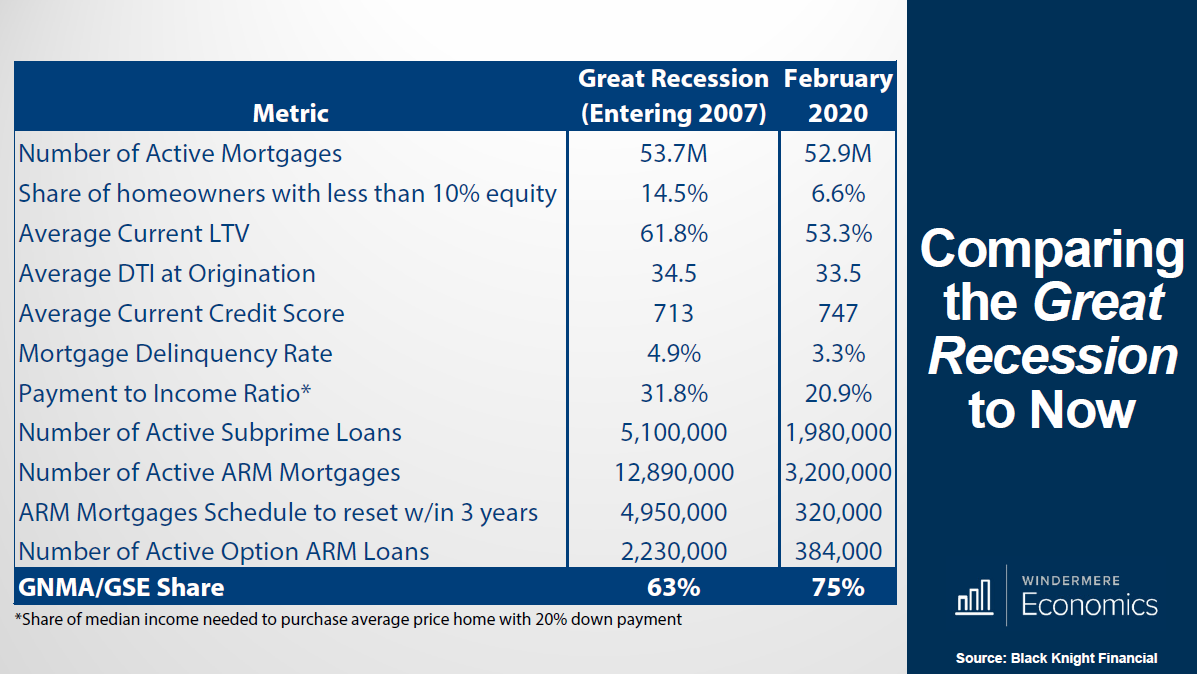

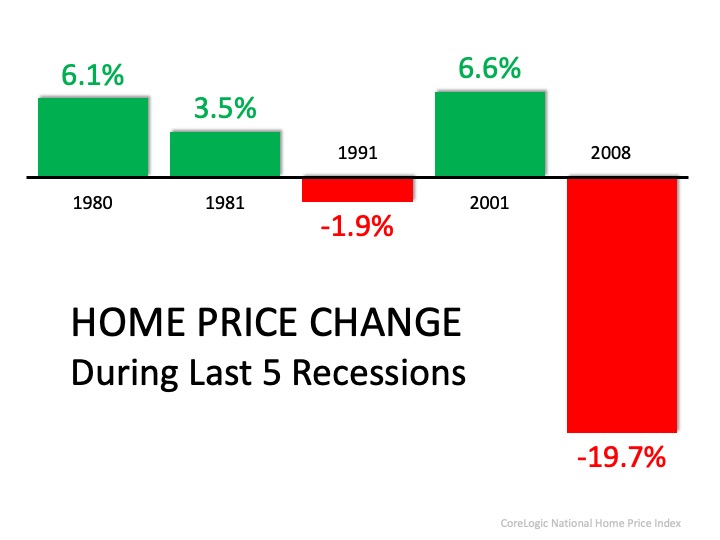

The effects of the COVID-19 pandemic have surely been felt economically. A common question that I have been asked is, “Is this 2008 all over again?” The answer is “No!” As Matthew touched on above, this is a health crisis, not a housing crisis. Yes, we are headed toward a recession, but not one that is based in housing like The Great Recession of 2008. That recession was primarily based on predatory lending practices that put people into homes they could not afford with little to no down payments and horribly vetted credit. In fact, of the last five recessions, three did not see price depreciation in housing.

Take a look at the graph to the right, which shows the homeowner households in King County with more than 50% equity in their home. In Q4 of 2019, 43% of homeowners in King County were in a very healthy equity position, owing less than 50% of what their home was worth. I have been tracking sales weekly since March 1st, and prices remain strong. We have a very limited amount of inventory, rates remain low, and buyer demand is being fueled by these positive components. Our economy was formidable prior to this, indicating solid bedrock for recovery once we weather this storm that needs to be waited out. The Greater Seattle Area is particularly fortunate as many of our large businesses are centered in information technology and Amazon, which have both stayed active during this time.

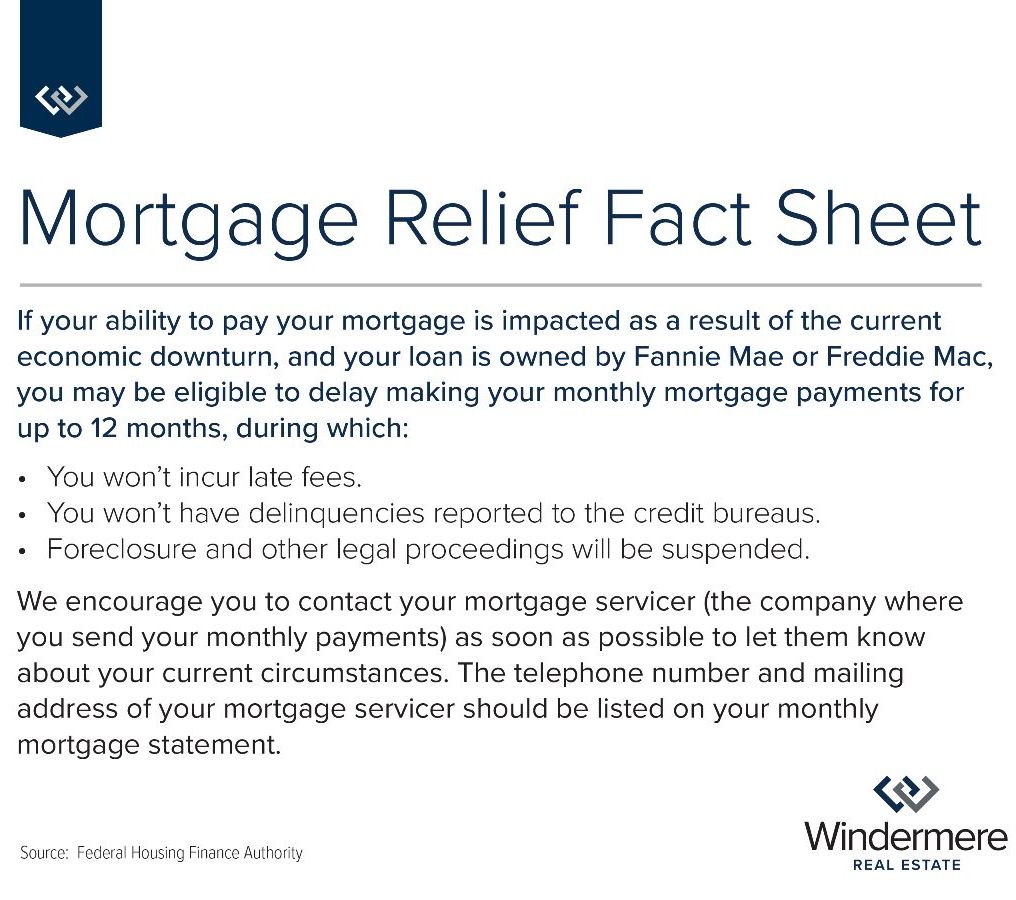

Another aspect that is different from the 2008 Great Recession is that some banks and mortgage investors (servicers) are working with homeowners to provide mortgage relief. With the shutdown of so many businesses and services, job losses have been abundant. If you or someone you know would benefit from setting up a mortgage forbearance program or loan modification in order to alleviate the pressure of monthly payments right now, click on this link and have them contact their mortgage servicer today. The available programs that are offered will vary from one loan servicer to another, and are primarily available for loans that are owned by Fannie Mae or Freddie Mac (click on the appropriate link to help research who owns your loan). Make sure you consider the details and payback terms for your long-term financial health. The ability to protect this asset while waiting this out will protect one’s equity. This is a milestone opportunity and will ensure a strong housing market moving forward.

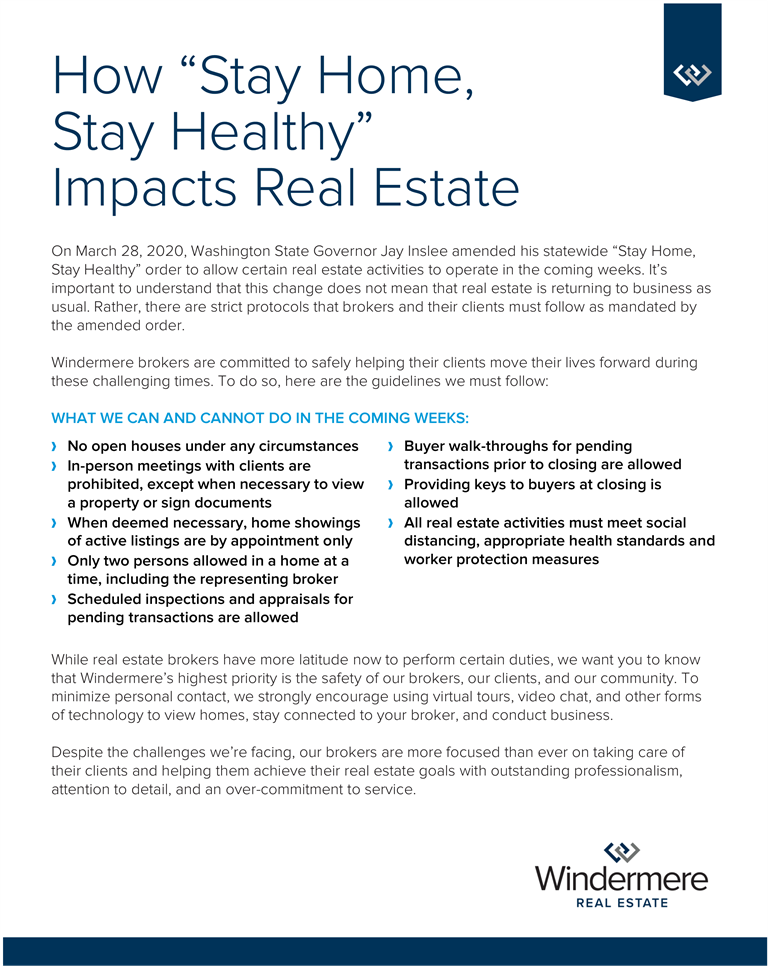

On Saturday, March 28th, Governor Inslee adjusted the Stay Home, Stay Healthy order in relation to how real estate services can be provided. The point of this was to get the 17,000 pending transactions in our state headed towards a successful close. This also opened up the option for real estate to transact in order to help homeowners who need to sell to become unstuck, and buyers who need housing to be placed. The adjustments were focused on creating safe housing and addressing economic needs. This is not business as usual and now more than ever, entering into a real estate purchase or sale takes a well-thought-out strategy. Public health and safety have become a part of that strategic plan and are of the highest priority to consider along with housing and financial needs. In fact, waiting it out will be the best choice for some. If you or someone you know needs some guidance or is in a position to buy or sell during the Stay Home, Stay Healthy orders, please reach out. Also, see below the restrictions that are in place to help ensure all of our safety.

The uncertainty of COVID-19 and all of its repercussions may leave you feeling helpless or anxious. Sometimes it might feel like the only thing we can do is stay home and wait. The good news is that there are some practical ways we can all help.

1. Give blood, if you can. Blood banks nationwide are in a state of crisis, with severe shortages due to an unprecedented number of blood drive cancellations. Even if your area has ordered residents to stay at home, going out to give blood is allowed as a volunteer activity to help meet essential needs. Go to Bloodworks Northwest or The American Red Cross to schedule an appointment.

*Blood banks are operating by appointment only to meet social distancing orders. Important note: Coronavirus has not been shown to be transmitted through blood transfusion.

3.Donate to health care workers. Now more than ever before, we need to support our front-line healthcare workers, who are so bravely fighting COVID-19 and taking care of our sick loved ones. Most hospitals have a donation page, outlining what they are currently in need of. Not only are they desperate for personal protection equipment such as gloves and masks, but many facilities are also accepting food (snacks for health care workers), notes of encouragement, or monetary donations. Do a quick search for the hospital nearest you to see what they are lacking and how you can help. Here are a few to get you started. UW Medicine Swedish Hospital Evergreen Hospital

4. Support local businesses. It is often said that small businesses are the backbone of America. Well, now is the time for us to rally and support the bedrock of our communities. Many restaurants are still open for take-out or delivery (have you tried Uber Eats, or Grubhub? These are great options, as you are not only supporting the corner pizza place, but the delivery driver as well), and many local shops are still selling online or offering curb-side pickup.

Some cities are rallying around their restaurants and shops by putting together a one-stop resource for who is open and what services are still available. I have linked a couple of local city’s lists below, including a very cool interactive map for the city of Seattle. For information on your city, try searching Facebook or looking up the city’s Chamber of Commerce website. Seattle Edmonds Bothell / Kenmore Everett

Take the challenge: the next time you think about ordering something on Amazon, stop and take a minute see if a local small business can fill that need for you instead.

Most recently, we have experienced an uptick in market activity. In fact, King County saw a 35% increase in pending sales from December to January, and Snohomish County 38%. The seasonal uptick from the holidays to the New Year is normal, but it was quite sizable. This is reinforced by a 6% increase in pending activity this January over last January in King County, and a 10% increase in Snohomish County. This increase is being driven by multiple factors, such as our thriving economy and growing job market, generational shifts and historically low interest rates.

Why is this important to pay attention to? Affordability! The Greater Seattle area is not an inexpensive place to own a home; we have seen strong appreciation over the last 7 years due to the growth of the job market and overall economy. The interest rate lasts the entire life of the loan and can have a huge impact on the monthly cash flow of a household. This cost savings is also coupled with a balancing out of home-price appreciation. Complete year-over-year, prices are flat in King County and up around 3% in Snohomish County. Note that from 2018 to 2019 we saw an 8% increase in prices in both King and Snohomish Counties. Price appreciation is adjusting to more normal levels and is predicted to increase 5-7% in 2020 over 2019.

As we head into the spring market, the time of year we see the most inventory become available, the interest rates will have a positive influence on both buyers and sellers. Naturally, buyers will enjoy the cost savings, but sellers will enjoy a larger buyer pool looking at their homes due to the opportunities the lower rates are creating. Further, would-be sellers who are also buyers that secured a rate as low as 3.75% via a purchase or refinance in 2015-2017, will consider giving up that lower rate for the right move-up house now that rates would be a lateral move or possibly even lower.

This recent decrease in rate is making the move-up market come alive. Baby Boomers and Gen X’er’s are equity rich and able to make moves to their next upgraded home or fulfill their retirement dreams. What is great about this, is that it opens up inventory for the first-time buyer and helps complete the market cycle. First-time buyers are abundant right now as the Millennial generation is gaining in age and making big life transitions such as getting married, starting families, and buying real estate.

Will these rates last forever? Simply put, no! Right now is a historical low, and depending on economic factors rates could inch up. According to Matthew Gardner, Windermere’s Chief Economist, rates should hover around 4% throughout 2020. While still staying well below the long-term average of 7.99%, increases are increases, and securing today’s rate could be hugely beneficial from a cost-saving perspective. Just like the 1980’s when folks were securing mortgages at 18%, the people that lock down on a rate from today will be telling these stories to their grandchildren. Note the long-term average – it is reasonable to think that rates closer to that must be in our future at some point.

So what does this mean for you? If you have considered making a move, or even your first purchase, today’s rates are a huge plus in helping make that transition more affordable. If you are a seller, bear in mind that today’s interest rate market is creating strong buyer demand, providing a healthy buyer pool for your home. As a homeowner who has no intention to make a move, now might be the time to consider a refinance. What is so exciting about these refinances, is that it is not only possible to reduce your monthly payment, but also your term, depending on which rate you would be coming down from. There are some pretty exciting money saving opportunities for people to take advantage of right now.

If you would like additional information on how today’s interest rates pertain to your housing goals, please contact me. I would be happy to educate you on homes that are available, do a market analysis on your current home, and/or put you in touch with a reputable mortgage professional to help you crunch numbers. Real estate success is rooted in being accurately informed, and it is my goal to help empower you to make sound decisions for your lifestyle and investment.

Celebrate Earth Day with us! We are partnering with Confidential Data Disposal for our 9th year; providing you with a safe, eco-friendly way to reduce your paper trail and help prevent identity theft.

Saturday, April 18th, 10AM to 2PM 4211 Alderwood Mall Blvd, Lynnwood

Bring your sensitive documents to be professionally destroyed on-site. Limit 20 file boxes per visitor.

We will also be collecting non-perishable food and cash donations to benefit Concern for Neighbors food bank. Donations are not required, but are appreciated.

Hope to see you there!

**This is a Paper-Only event. No x-rays, electronics, recyclables, or any other materials.

It’s a great time to begin preparing your home for spring. Here are a few general home maintenance tips to consider this time of year.

Clean the kitchen exhaust hood & filter.

Replace the furnace filter. It may be especially filthy after the winter months.

Inspect the roof for water damage. It’s also a good idea to check any fences, carports and sheds. TIP: check the south end of your roof first; it is the first to show wear.

Test the batteries in all smoke and carbon monoxide detectors.

Clear the gutters of any buildup to allow for proper functioning.

Start the grass revival cycle by aerating, thatching and fertilizing.

Be sure no inside or outside vents are blocked by fallen debris.

Clean the windows and screens. Repair any holes in screens or replace them if needed.

Inspect and repair siding and peeling paint. Fix or replace damaged siding. Strip peeling paint and replace it with a new coat.

Check the basement for water damage. Pay attention to musty smells, water stain and damp surfaces.

Invest in a carbon monoxide detector – every home should have at least one.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Take a look at the graph to the right, which shows the homeowner households in King County with more than 50% equity in their home. In Q4 of 2019, 43% of homeowners in King County were in a very healthy equity position, owing less than 50% of what their home was worth. I have been tracking sales weekly since March 1st, and prices remain strong. We have a very limited amount of inventory, rates remain low, and buyer demand is being fueled by these positive components. Our economy was formidable prior to this, indicating solid bedrock for recovery once we weather this storm that needs to be waited out. The Greater Seattle Area is particularly fortunate as many of our large businesses are centered in information technology and Amazon, which have both stayed active during this time.

Take a look at the graph to the right, which shows the homeowner households in King County with more than 50% equity in their home. In Q4 of 2019, 43% of homeowners in King County were in a very healthy equity position, owing less than 50% of what their home was worth. I have been tracking sales weekly since March 1st, and prices remain strong. We have a very limited amount of inventory, rates remain low, and buyer demand is being fueled by these positive components. Our economy was formidable prior to this, indicating solid bedrock for recovery once we weather this storm that needs to be waited out. The Greater Seattle Area is particularly fortunate as many of our large businesses are centered in information technology and Amazon, which have both stayed active during this time.